The interest Rate and Inflation Tug-of-War

Contributing Author: Elite Wealth Management

Welcome to our latest market outlook written by our financial partner at Elite Wealth Management.

Their in-depth analysis and insights into the interest rate and inflation tug-of-war are incredibly informative, making it a must-read for both seasoned investors and those new to the world of finance.

At Unikorn, we believe in making Commercial Property easy and accessible for everyone. That’s why we’re here to answer any questions you may have.

So, if you have any questions or need further clarification on any of the topics covered in this article, please feel free to reach out to us at helen@unikorn.com.au.

We’re excited to share this informative article with you, and we hope you find it valuable as you navigate the complex world of finance.

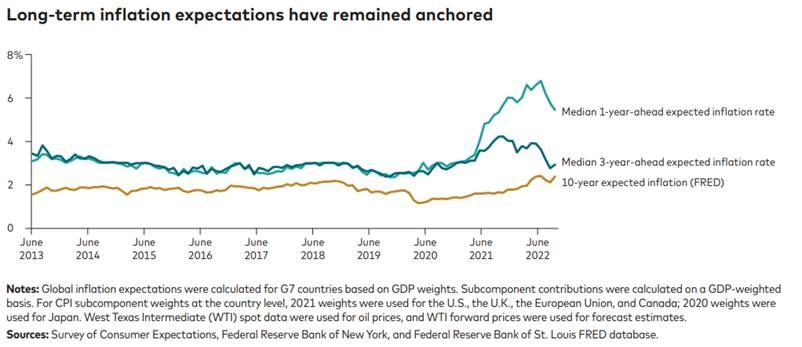

Inflation Expectations

- Inflation expectations have largely remained anchored

Inflation expectations have largely remained anchored – especially those that look out over longer periods. Should this change, central banks will increase the urgency of their tightening process.

- Central Bank Credibility

Central banks have built up credibility regrading their resolve and ability to keep inflation at target rates (i.e. the efforts to bring down inflation and maintain it around 2% for the past 30 years). The credibility gained has helped inflation remain anchored (see above) but is also the key reason why the likelihood of central banks changing their inflation targets in the middle of a high inflation environment remains low for now (as doing so could hurt their credibility to address inflation in future).

As a consequence of rising rates, global financial conditions continue to tighten, as shown in the financial conditions index below.

Market Outlook

Employment markets remain strong with more jobs available than people to fill them, which underpins our expectations for a ‘job-full’ recession, which may be relatively shallow (akin to 2001).

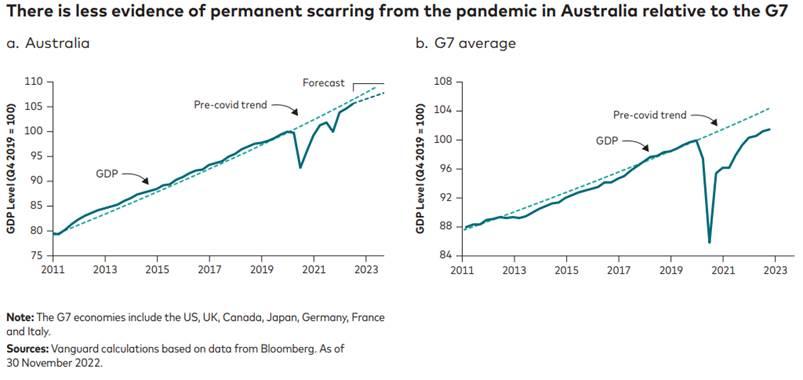

Australia: Better placed to ride out the storm…

Australia has bounced back strongly from the pandemic, supported by low interest rates, generous government spending, and the release of pent-up demand which has boosted consumer spending. In fact, Australian GDP is only 1% below its pre-covid trend, suggesting only modest permanent scarring from the pandemic.

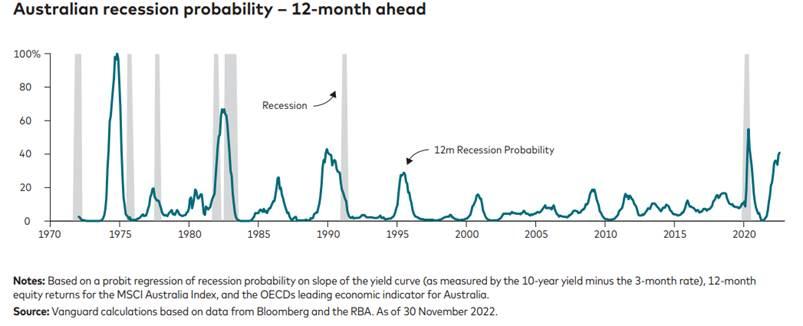

…but recession risks rising

Our recession probability model, which captures three key leading indicators of recession including the slope of the yield curve, equity market returns and leading economic indicators, is currently around 40%, suggesting that the chances of recession are material in 2023.

Despite these warning signals, Australia has a better chance than most advance economies to avoid recession. This is due to several factors.

- Australia being a net exporter of commodities and stands to benefit from surging commodity prices.

- As China relaxes zero Covid policy, Chinese activity will rebound, supporting Australian exports.

- Inflation has not reached the same levels as other advanced economies so interest rates may not need to rise as far.

- Wage growth remains modest in Australia (3.1% in September). Trade unions have failed to negotiate large wage increases for workers under enterprise bargaining agreements (which accounts for 40% of workers) so a wage inflation spiral is less likely.

Given that inflation is still well above target, we expect the RBA to continue raising interest rates to around 4.35%. We forecast inflation to peak at around 8% in coming months and fall back to 4.5% by the end of 2023.

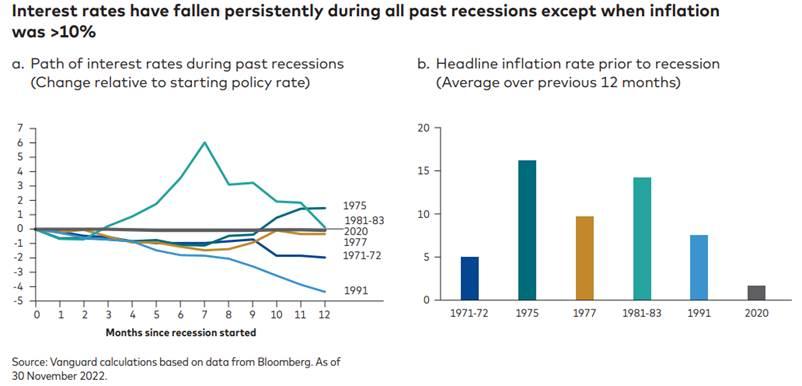

Will there be rate cuts in 2023?

2023 will be a challenging year for the RBA, who will face a difficult trade-off between dampening inflation and averting recession. If the economy does fall into a recession the RBA may feel compelled to cut interest rates. Indeed, when we look back at recessions over the past 50 years, we observe that the RBA cut rates in every single recession (see below). Although they quickly raised rates during the recessions of 1975, 1977 and 1981-83, given inflation was at or above 10%. The key lesson we believe that the RBA took from these experiences is that cutting rates during recessions leads to even higher inflation, and an even longer battle to bring inflation back down.

Therefore, we believe rate cuts are less likely in 2023.

2023 – a break in the clouds?

The stormy weather experienced by financial markets 2022 has likely unsettled even the most seasoned of investors. Indeed, the last time we saw US stocks and bonds contract more than 10% concurrently, was in the early 1800s – almost the era of Alexander Hamilton!

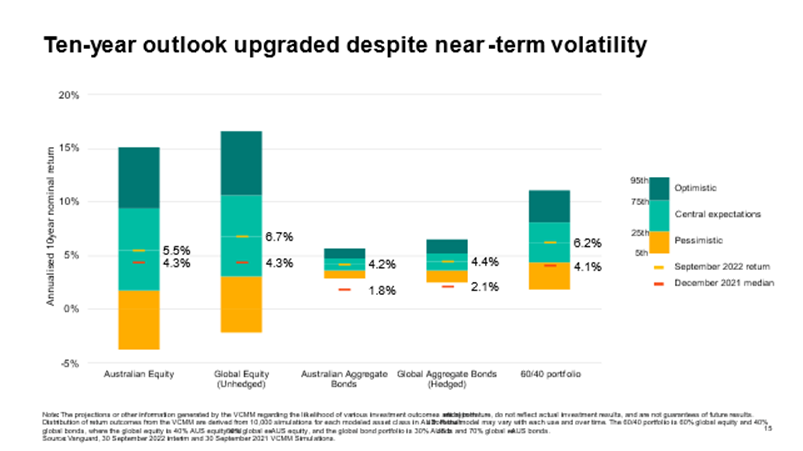

However, the silver lining is that both equities and fixed income are now a lot more attractively priced than where we were at the end of either 2020 or 2021. In recent years, Vanguard’s Global Chief Economist had described the outlook for markets as ‘guarded’ or ‘muted’ as increasingly stretched bond and equity valuations tempered expectations of future returns. Despite the backdrop of recession in 2023 for many major economies, the good news is that the outlook for markets for the next decade is more ‘formative’.

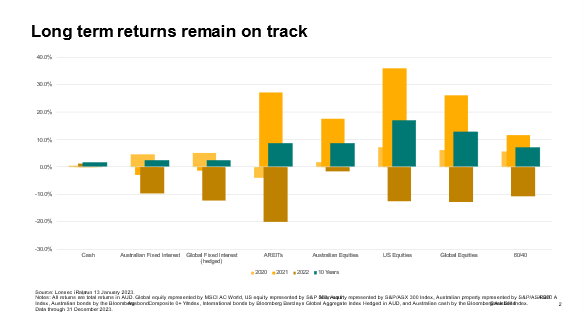

We know that in the long run, markets deliver but the journey can be bumpy. While 2022 was a challenging year its important to remember that 2020, even with the March 2020 volatility delivered solid gains and 2021 was quite a strong year – albeit powered by fiscal support. The chart below shows the prior three years annual calendar returns in the yellow shades, alongside the returns for the decade ending December 2022.

Interestingly the last decades returns for the 60/40 portfolio (7.1%) are not all that far off the 6% to 7% range we expect for the next decade!

Global capital markets outlook

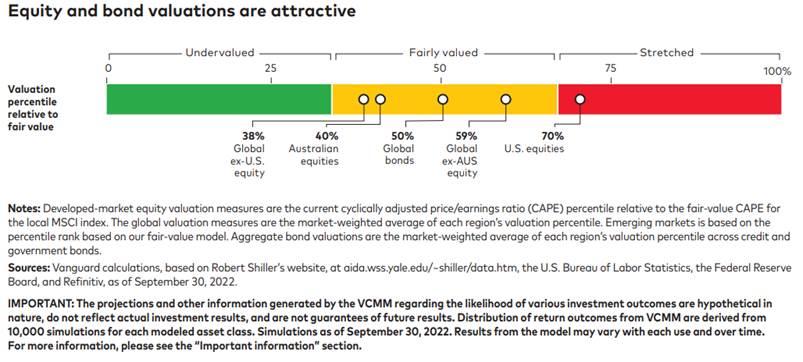

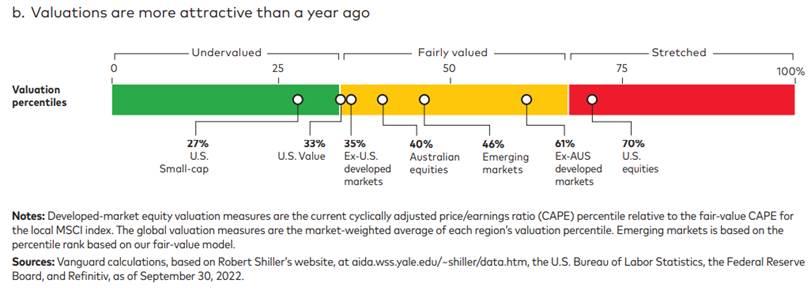

Although it is impossible to say with confidence when equity and bond markets will bottom, valuations and yields are clearly more attractive than they were a year ago. Looking ahead, our return outlook—which has been on a steady downward trajectory since 2009—is ticking up. In equities, global valuations are more attractive than they were last year, but are still above our estimate of fair value in certain regions.

Global fixed income: Brighter days ahead

The market, which was initially slow to price higher interest rates to fight elevated and persistent inflation, now believes that most central banks will have to go well past their neutral policy rates—the rate at which policy would be considered neither accommodative nor restrictive—to quell inflation. In Australia, we expect the cash rate to reach 4.35% by mid-2023, higher than currently anticipated by markets and economists, given the RBA’s strong desire to quash inflation.

Although rising interest rates have created near-term pain for investors, higher starting interest rates have raised our return expectations significantly for global bonds. We now expect Australian bonds to return 3.7%–4.7% per year over the next decade, compared with the 0.9%–1.9% annual returns forecast a year ago. For global bonds, we anticipate returns of 3.9%–4.9% per year over the next decade, compared with our year-ago forecast of 1.3%–2.3%.

Vanguard’s Global Head of Fixed Income (Sara Devereaux) recently shared four things to keep in mind regarding fixed income.

- Valuations are materially better – yields are now the best they have been for a decade.

- Income is back! The healthier coupon which delivers income on bonds, underpins the stable component of fixed income returns

- Diversification benefits are also back

- During recessionary periods (like the conditions we are likely to encounter in 2023), bonds tend to do relatively well.

Although rising interest rates have created near-term pain for fixed income investors, we expect that those with sufficiently long investment horizons will be better off in end-of period wealth terms by the end of the decade than if they had just realised our return forecast from the end of last year. This is because of the effect of duration.

When interest rates rise, bonds reprice lower immediately. However, cash flows can then be reinvested at higher rates. Given enough time, the increased income from higher coupon payments will offset the price decline, and an investor’s total return should increase.

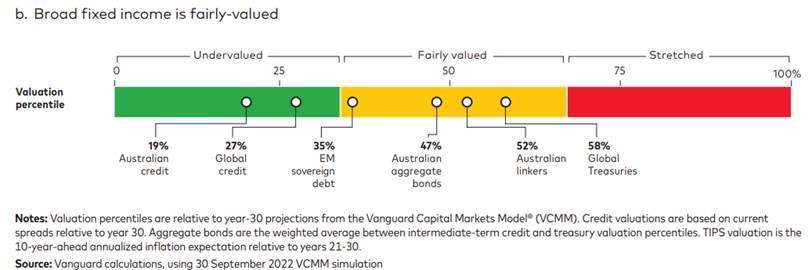

Australian and global credit attractively valued

Despite a record pace of policy tightening and a historic rise in government bond yields in 2022, credit spreads have remained remarkably resilient. Both investment grade and high-yield spreads are most sensitive to economic conditions, but the slope of the yield curve matters more for investment-grade than for high-yield, whereas, high-yield is more sensitive to corporate debt fundamentals given its riskier credit profile.

Although both investment-grade and high-yield bond spreads are within our fair-value range, it is reasonable to expect that they could widen more given our outlook for weaker economic conditions, high short-term interest rates to fight inflation, and slower corporate profit growth.

Given the material increase in base government bond rates and relatively conservative positioning of Global Active Credit, it might be worth considering in 2023. Rising coupons have transformed expected return calculations and brought back the long-established use case of bonds within the context of the asset allocation of balanced portfolios.

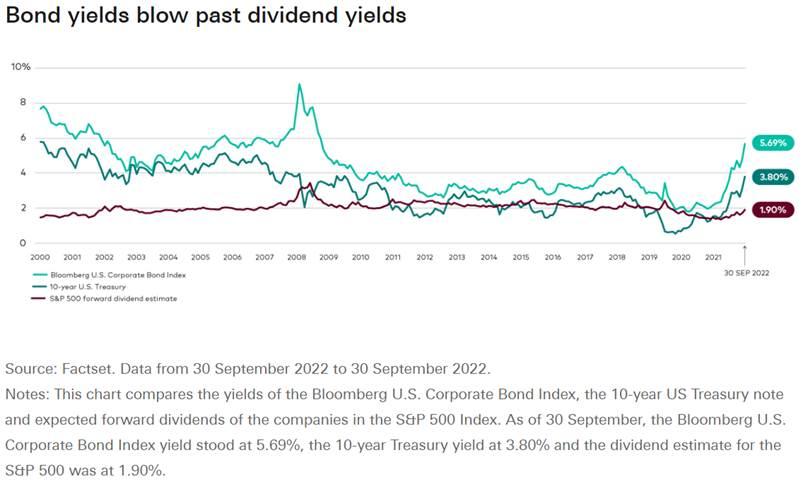

Comparing the dividend yield on the S&P 500 against the yield on US Treasuries shows just how far we’ve come this year. While many investors have implemented new, more esoteric positions in search of yield or uncorrelated assets—such as in private credit—it seems an opportune time to reconsider an old-fashioned, long-term asset allocation.

Equity valuations more favourable

The sell-off in equity markets this year has been widespread, with many equity indexes posting losses greater than 20% in the last nine months. Valuation declines were more pronounced in U.S. markets, but a weakening Australian dollar meant Australian investors realised smaller losses on their unhedged international equity exposures than suggested by local currency performance. Even though these losses are significant from a short-term, realised-return perspective, it means that the global opportunity set is now more attractive than it was a year ago.

In any portfolio, there are benefits to be gained by considering a diversified approach to investments. Holding all assets in one sector can void your portfolio of the benefits of liquidity and a multi-pronged approach to investments and flexibility. Furthermore, the structuring and ownership of your investments can play an important role in your current and future outcomes after tax. It is equally important to consider what ownership structure will meet your short and long term goals.

We suggest a review with your Financial Adviser and Accountant to consider and determine what is the best way for you to diversify to meet your goals and what is the best ownership structure taking into account short, medium and long term plans for your investments.

Please contact us on 1300 ELITE 0 to take advantage of your complimentary health check.

This information is current as at February 2023 and is subject to change. As this information (including the statements on taxation which are of a general nature only and based on current laws, rulings and interpretation) has been prepared without considering your objectives, financial situation or needs, you should, before acting on this information, consider its appropriateness to your circumstances. Elite Wealth Management is a corporate authorised representative of PGW Financial planning (AFSL 384713). You should consult with your financial adviser before selecting any insurance or investment products. The information provided in this article is general in nature and any personal advice to meet your personal objectives would need to be provided on an individual basis.

Elite Wealth Management (AR 1296131 ABN 50688637647) is a Corporate Authorised Representative of PGW Financial Services Pty Ltd (AFSL 384713 ABN 15 123 835 441). Jolene Sukkarieh (AR 300103) is an Authorised Representative of PGW Financial Services Pty Ltd AFSL 384 713 ABN 15 123 835 441

References:

https://trilogyfunds.com.au/investing/trilogy-industrial-property-trust/

https://reia.com.au/wp-content/uploads/2023/02/REIA-MEDIA-RELEASE_LENDING-STATS_030223.pdf

https://www.vanguard.com.au/institutional/insights/en/markets-economy

Recent Deals:

Garbutt, QLD

Purchase Price: $817,000

Yield: 7.32%

Positive Cashflow: $18,936

Currajong, Townsville

Purchase Price: $900,000

Yield: 8.51%

Positive Cashflow: $31,545

Cashed Up Book

Testimonials

“We wanted to say a BIG thank you to Helen and her team of professionals. We were very nervous getting into the commercial space as it was unknown territory for us. Helen understood what we required for our strategy and made it happen. Her team of professionals range from loan specialists, solicitors, due diligence team and commercial experts. This made our journey

from the beginning (putting an offer down) all the way to settlement, very smooth and gave us confidence.

Would not hesitate to highly recommend Helen to anyone that is looking to embark in the commercial

space and we are looking forward to our next deal with

Testimonials

“Right from the beginning with strategy planning Helen has guided us in a professional manner. Her team has been very helpful in explaining the due diligence process to novices like us. We are very happy with our first commercial property purchase yielding 7%. Could not have done that without Helen and her team. We are looking forward to building our portfolio with more purchases like these. The great aspect of this experience has been the fact that we could always access Helen and her team at short notice for even minute questions.”

Testimonials

“It’s been a great experience working with Helen in purchasing my second commercial property. The previous buyer’s agent I engaged with has good reputation in the market but could not find me a property for almost 4 months, so I decided to go with Helen. Helen was very efficient in finding me a great property. Huge thanks to Helen and her team for all the work you’ve done in the whole process. Will definitely purchase more with you in the future!”

Testimonials

“Helen and her team did a wonderful job. The whole process was taken care of. Everything from lease and building DD to finance was all handled quickly and professionally.

Thanks again to all of you. I’m looking forward to the next deal.”